How Ad Agencies Get Approved for Higher Credit Limits Without a Personal Guarantee

TL;DR

Most business credit cards require a personal guarantee, which means the agency owner is personally liable for ad spend charged to client budgets they do not control.

Traditional card issuers cap limits based on the agency's own revenue and credit profile, not on client budget size, creating a structural ceiling that limits how many clients an agency can scale.

The Client-Funded Card model, used by Opal Spend, removes personal liability by having clients pre-fund the card before spend occurs, eliminating the credit risk that makes personal guarantees necessary in the first place.

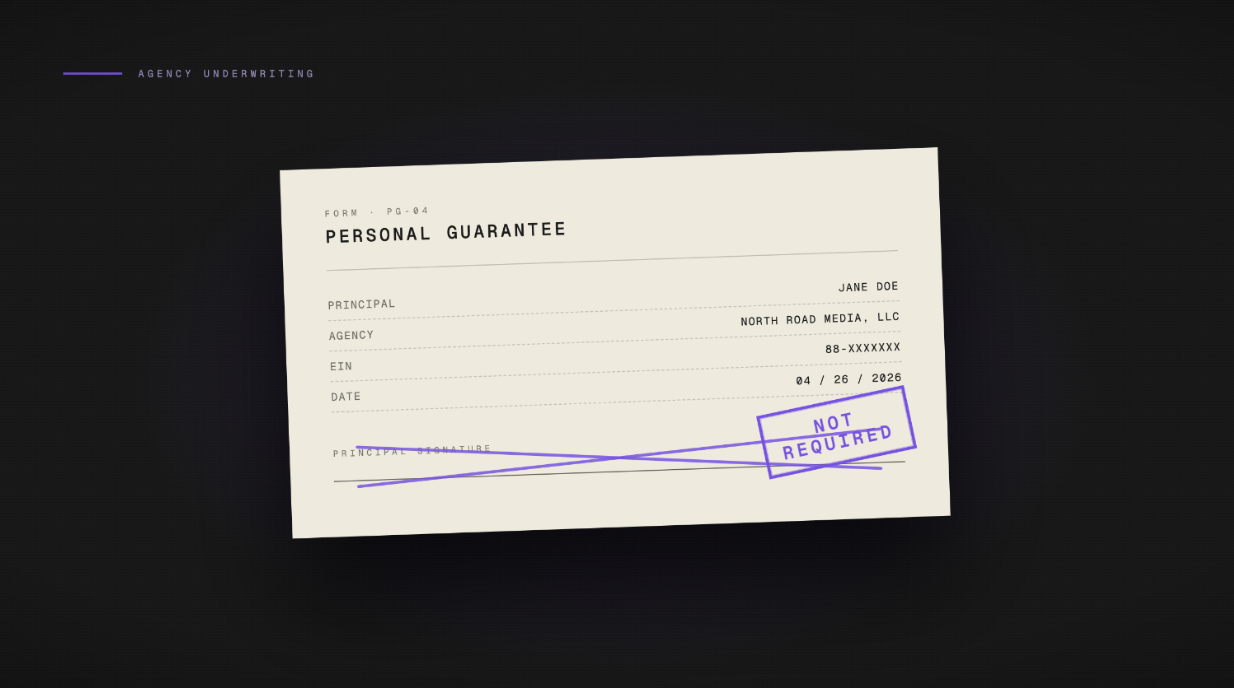

Opal Spend offers ad agencies credit limits up to $10M, requires no personal guarantee, performs no hard credit check, and can approve an agency in 2 to 3 minutes.

Executive Summary

Most business credit cards were designed for companies spending their own money. When an agency applies for a card to manage client ad budgets, it runs headfirst into underwriting logic that was never built for that use case. The result: personal guarantee requirements, hard credit pulls, and limits that cap out well below what the agency actually needs to operate.

For agencies running $100K, $500K, or $1M+ in monthly ad spend, this is not a minor inconvenience. A personal guarantee means the agency owner is personally on the hook for every dollar charged to that card, including client budgets the agency never controls and never profits from. The fix is not a higher limit on the same flawed model. It is a different model entirely.

The Wall Every Growing Agency Hits

The pattern is consistent. An agency lands a new client with a $150K monthly ad budget. The owner applies to increase their business card limit to cover it. The card issuer comes back with one of three responses: sign a personal guarantee, submit to a hard credit check that may not even result in the limit needed, or get approved for a fraction of what was requested.

So the agency owner signs the guarantee, takes the inquiry hit, and moves on. Then it happens again with the next client. And the next.

The three consequences that compound over time:

-

Personal credit exposure. Every hard inquiry, every high utilization rate on a card tied to client spend, and every missed payment that traces back to a client's delayed wire lands on the owner's personal credit report.

-

Liability for spend you never benefit from. The agency earns a management fee. The client owns the budget. But if a client pulls their contract mid-month with $80K already spent on ads, the agency owner is personally liable for that balance.

-

A growth ceiling disguised as a credit limit. When the card limit is $25K and the next client needs $200K in monthly ad spend, the card is not a tool anymore. It is a constraint on how large the agency can grow.

Why Traditional Business Cards Require a Personal Guarantee

Personal guarantees exist because card issuers need a fallback when a business cannot pay. For most businesses, especially small ones, the business and its owner are financially intertwined. If the business fails, the issuer needs recourse. Tying repayment to the owner's personal assets is a straightforward solution to that risk.

This underwriting model made sense when it was designed. A small business owner buying inventory, paying contractors, or covering operating expenses is spending money the business generates or intends to generate. The card issuer is essentially underwriting the business's ability to repay from its own cash flow.

Why This Model Was Not Built for Agencies

Digital marketing agencies operate on a fundamentally different financial structure. They are not spending their own money. They are spending client money, on behalf of clients, to run campaigns that the client owns and controls. The agency's revenue is a management fee, not the ad spend itself.

Traditional card issuers do not distinguish between these two models. When an agency applies for a business card, the underwriting process evaluates the agency's own revenue, credit history, and assets, not the client budgets the card will actually be used to manage. The result is a limit calibrated to the wrong number.

The underwriting gap in one sentence: a card issuer looks at a $500K/year agency and sets a $30K limit, while that same agency manages $2M/year in client ad budgets that flow through that card every month.

The Asymmetric Risk Problem Unique to Ad Agencies

When a company spends its own money on a business card, the risk is symmetric. If the company cannot pay, it is because the company's finances failed. The personal guarantee ties the owner to their own business's performance.

For an agency, the risk is asymmetric by design. The agency carries the liability. The client owns the budget. The card issuer gets paid either way.

Consider what this means in practice:

Party |

Role |

Risk Exposure |

|---|---|---|

Agency owner |

Signs personal guarantee |

Personally liable for full balance |

Client |

Controls and owns the budget |

Zero liability; can cancel at any time |

Card issuer |

Processes transactions |

Protected by personal guarantee |

The agency is the only party in this arrangement that bears financial risk for money it does not own. If a client is slow to wire their monthly budget, the agency owner is personally exposed for the gap. If a client disputes charges or cancels mid-cycle, the card balance does not disappear with them.

This is not a hypothetical edge case. It is the standard operating condition for any agency that runs client ad spend through a card tied to a personal guarantee. The larger the client budget, the larger the personal exposure.

What Agencies Do to Work Around This (And Why It Fails)

Agencies have developed a set of workarounds for the credit limit problem. None of them solve it. They each introduce new operational problems that compound over time.

Stacking Multiple Business Cards

Applying for cards from several issuers to aggregate limit capacity is common. The problems: each application triggers a hard credit inquiry, high utilization on any single card drags down the owner's credit score, and reconciling spend across five cards for ten clients creates a bookkeeping burden that scales badly.

Using Personal Cards

Some agency owners run client ad spend on personal cards to access higher limits or better rewards. This co-mingles business and personal finances, creates a tax and accounting headache, and still exposes personal credit. It also caps out the same way once personal limits are reached.

Rotating Balances and Timing Payments

Agencies that run close to their limits often time payments manually to free up capacity before the next billing cycle. This works until a client's wire is delayed, a platform charges earlier than expected, or a campaign scales faster than anticipated. One mistimed payment can pause campaigns mid-flight.

Asking Clients to Run Their Own Cards

Having clients use their own payment methods eliminates agency liability but also eliminates agency control. Re-verification issues become the client's problem to solve. Reconciliation requires pulling data from the client's account. And the agency loses visibility into spend it is responsible for managing.

The pattern across all workarounds: they trade one problem for a different one. None of them address the structural mismatch between how agencies operate and how traditional card underwriting works.

How the Client-Funded Card Model Changes the Underwriting Equation

The reason personal guarantees exist is credit risk: the issuer needs assurance that the balance will be repaid. Remove the credit risk, and the personal guarantee becomes structurally unnecessary.

The Client-Funded Card model does exactly that. Instead of the agency spending on credit and repaying later, the client pre-funds the card before spend occurs. The money is already there before a single dollar goes to Google Ads or Meta. There is no balance to guarantee because there is no credit extended in the traditional sense.

Why This Changes What the Issuer Can Offer

When spend is pre-funded by the client, the underwriting equation changes at its foundation:

The issuer is not extending credit against the agency's future revenue

The agency is not borrowing against its own assets

The client budget, not the agency's credit profile, determines the available limit

This is what allows Opal Spend to offer credit limits up to $10M without requiring a personal guarantee or running a hard credit check. The risk profile that necessitates those requirements in the traditional model simply does not exist in the same form here.

The practical result: an agency's credit limit with Opal scales with its client budgets, not with the owner's personal credit score. An agency managing $800K in monthly client ad spend can access limits calibrated to that number, not to the agency's own balance sheet.

What the Approval Process Actually Looks Like With Opal

The contrast between applying for a traditional business card and applying for Opal is significant enough to be worth stating explicitly.

Traditional Business Card Application

-

Timeline: 2 to 4 weeks for approval decisions, often longer for higher limits

-

Requirements: Personal guarantee from the business owner, hard credit check, business financials, sometimes personal tax returns

-

Limit logic: Based on the agency's own revenue and credit profile, not client budgets

-

Outcome: A limit that may be a fraction of what the agency needs, tied to personal liability

Opal Application

-

Timeline: 2 to 3 minutes

-

Requirements: No personal guarantee, no hard credit check

-

Limit logic: Tied to client budgets, not the agency's personal credit profile

-

Maximum limit: Up to $10M

-

Annual fee: None

The application process at Opal does not require an agency owner to put personal assets on the line or wait weeks for a decision. An agency can apply, get approved, and start issuing virtual cards to ad platforms the same day.

Opal also auto-syncs with Google Ads, Meta, TikTok, Snapchat, LinkedIn, Amazon, and The Trade Desk. This prevents the re-verification loops that cause campaign interruptions when a card number changes or a limit is hit mid-cycle. Unlimited free virtual cards mean each client or campaign can have its own dedicated card, keeping spend separated without requiring multiple accounts or card issuers.

Who This Matters Most For

Not every agency feels this problem at the same time. The inflection point is usually tied to a specific moment: a new client that breaks the current card setup, a personal guarantee that finally feels too large to sign, or a growth rate that the existing credit infrastructure simply cannot support.

The Agency Adding a New Enterprise Client

An agency's current card has a $50K limit. A new enterprise client comes on with a $200K monthly ad budget. The agency cannot run that client's spend on its existing card, cannot get the limit increased without a personal guarantee, and cannot afford the 2 to 4 week approval window while the client expects campaigns to launch. This is the scenario where a 2 to 3 minute approval with no personal guarantee changes everything.

The Agency Running Seven-Figure Monthly Spend Across Multiple Clients

An agency managing $1M+ in monthly ad spend across 10 clients has already exhausted what traditional cards can offer. The limits are too low, the reconciliation is a mess, and the personal guarantee exposure has become material. What this agency needs is a single card infrastructure that scales to the full book of business, with per-client virtual cards and automatic reconciliation built in.

The Agency Owner Who Has Maxed Personal Limits

Some agency owners reach the point where they are rotating balances across personal cards, timing payments manually, and watching their personal credit score move with client spend patterns they do not control. This is the most acute version of the problem. The solution is not a higher personal limit. It is removing personal credit from the equation entirely.

The common thread: in each scenario, the card is not a financial tool anymore. It is the ceiling on growth. Removing the personal guarantee and scaling the limit to client budgets turns it back into a tool.

Frequently Asked Questions

Can an ad agency get a business credit card without a personal guarantee?

Yes. Opal Spend is a charge card built exclusively for digital marketing agencies. It requires no personal guarantee. The card uses a Client-Funded Card model in which client budgets pre-fund the card before spend occurs, removing the credit risk that makes personal guarantees necessary in traditional underwriting. Agencies can apply and get approved in 2 to 3 minutes with no hard credit check.

How do agencies get high credit limits for ad spend?

Agencies get high credit limits for ad spend by using a card whose limits are tied to client budgets rather than the agency's own revenue or credit profile. Opal Spend offers limits up to $10M for agencies, calibrated to the actual client budgets being managed rather than the agency's balance sheet. Traditional business cards from general-purpose issuers cap limits based on the agency's own financials, which typically produces limits far below what the agency needs to manage client ad spend.

What credit limit does an agency need to run ads for multiple clients?

The required credit limit depends on the aggregate monthly ad spend across all clients. An agency running $50K per month per client across 10 clients needs a card infrastructure that supports at least $500K in monthly capacity, ideally with per-client virtual cards to keep spend separated. Opal Spend supports this with limits up to $10M and unlimited free virtual cards, allowing agencies to issue a dedicated card per client or campaign.

Does Opal Spend require a personal guarantee?

No. Opal Spend does not require a personal guarantee from agency owners. This is a stated feature of the product, not an exception or a promotional offer. The no-personal-guarantee policy applies to all agencies using Opal's Client-Funded Card model, regardless of the agency's size or credit history.

Does Opal Spend run a hard credit check during the application?

No. Opal Spend does not perform a hard credit check as part of the application process. The application takes 2 to 3 minutes and does not impact the applicant's personal credit score. Credit limits are determined by client budget size, not by the agency owner's personal credit profile.

How can an agency scale ad spend without personal liability?

An agency can scale ad spend without personal liability by using a card model that does not tie repayment to the agency owner's personal assets. With Opal Spend's Client-Funded Card model, clients pre-fund their ad budgets before spend occurs. Because the money is already on the card before a campaign runs, there is no outstanding balance for the agency owner to be personally liable for. This allows agencies to scale spend to client budget levels, up to $10M, without signing a personal guarantee.

What happens if a client cancels mid-month with ad spend already charged?

With a traditional card tied to a personal guarantee, the agency owner remains personally liable for any outstanding balance, including spend charged on behalf of a client who has since canceled. With Opal's Client-Funded Card model, client budgets are pre-loaded before spend occurs, which means the funds are already present before campaigns run. For details on how balance policies apply to specific situations, agencies should review Opal's terms at opalspend.com.

If your current card setup is limiting how many clients you can take on, or you have signed a personal guarantee you were not comfortable with, Opal Spend was built for exactly this situation. No personal guarantee. No hard credit check. Limits up to $10M tied to your client budgets. The application takes 2 to 3 minutes.