Why Are My Ad Spend Rewards Lower Than Expected?

You did the math when you signed up. At $X per month in ad spend, multiplied by the advertised cashback rate, the annual reward looked meaningful. Then the statements started coming in and the number didn't match.

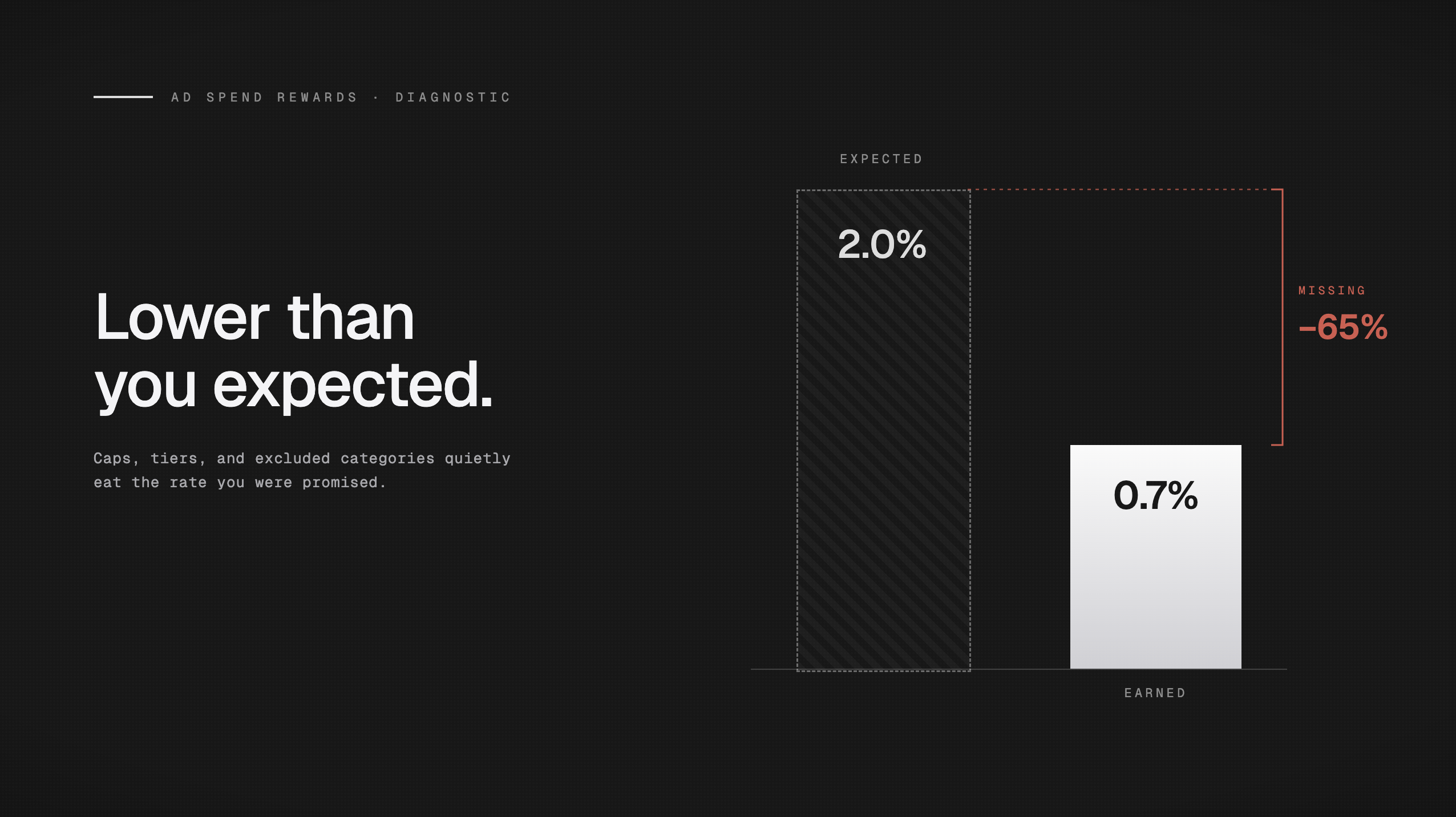

You're not miscalculating. The gap between what was advertised and what lands in your account is real, and it's not a mistake on your part. It's the structure of most reward programs working exactly as designed.

TL;DR

Most ad spend reward programs advertise a best-case rate that the majority of users never actually hit. Six specific mechanisms create the gap: spend caps, merchant category code mismatches, conditional rate requirements, payout delays, spend dilution from non-ad purchases, and points-versus-cash redemption discounts. If your ad spend rewards are not adding up, one or more of these is almost certainly the reason.

Reward programs are built to advertise the ceiling, not the floor. The headline rate is real, but it applies under specific conditions that are buried in the terms. Most cardholders live somewhere between the floor and the ceiling without ever understanding why. This post explains every mechanism that pushes you down from the advertised rate so you can find your specific answer quickly.

Reason 1: You Hit a Spend Cap Without Realizing It

This is the most common reason cashback caps on business cards catch people off guard. Most business cards that offer elevated rewards on advertising or office expenses apply those rates only up to a specific annual or quarterly spend threshold. Once you cross it, every dollar above the cap earns at the base rate, which is typically 1% or lower.

The math is straightforward once you know the cap exists. If your card caps bonus-category rewards at $150,000 per year and you run $50,000 per month in ad spend, you hit that ceiling in three months. For the remaining nine months of the year, you earn the base rate on every dollar, not the bonus rate you were counting on.

What this means in practice: A card advertised at 3% on advertising that caps at $150k/year delivers a blended rate of roughly 1.5% for an agency running $50k/month. The 3% headline is technically accurate. The effective annual rate is not.

To find your own cap: pull up your card's rewards terms and search for "bonus category limit," "annual cap," or "quarterly maximum." The cap number is almost always there. Divide it by your monthly ad spend to see how many months you actually earn the headline rate.

Reason 2: Your Ad Spend Doesn't Qualify as the Bonus Category

Many cards offer elevated rewards on "advertising" as a bonus category. The catch: whether a transaction qualifies as advertising depends entirely on the merchant category code (MCC) assigned to the vendor by the card network, not on what the purchase actually is.

Ad platforms do not always code as "advertising." Meta, Google, TikTok, and other platforms have been assigned various MCCs over time, including codes that fall under "computer services," "online services," or "data processing." If your card's bonus rate applies specifically to the advertising MCC (typically 7311) and your ad platform codes differently, that spend earns the base rate regardless of what you're buying.

The result: Your card technically offers 3% on advertising. Your Meta and Google spend codes as something else. You earn 1% on the majority of your ad budget and never understand why.

This is genuinely difficult to verify in advance because MCC assignments can vary by issuing bank and occasionally change. The only way to confirm is to run a small test transaction and check how it categorizes on your statement, or contact your card issuer directly and ask which MCCs qualify for the advertising bonus category.

If you're trying to find a card where your actual ad platform spend reliably earns the bonus rate, the best credit card for online advertising post covers this in detail.

Reason 3: The Headline Rate Requires Conditions You Haven't Met

Some cards advertise a headline rate that is technically achievable but only under a specific combination of conditions. The 3% or 4% number in the marketing is real. The terms required to unlock it are not always obvious at signup.

Common conditions that gate the headline rate:

-

Pre-funding a cash account with the card issuer before transactions post

-

Enrolling in an instant payout or accelerated payment program that changes how your billing cycle works

-

Maintaining an active referral program with a minimum number of referred accounts

-

Hitting a loyalty spend tier within a rolling time window

-

Paying a monthly or annual fee that was not prominently disclosed alongside the rate

When a card requires multiple simultaneous conditions to unlock its top rate, most users default to a lower base rate without realizing the headline rate was conditional. The advertised number was never wrong. It just wasn't describing the experience most users actually have.

Before signing up for any card with a high headline rate: ask the issuer directly what the base rate is if you do nothing beyond using the card. That number is your realistic starting point. The headline rate is the ceiling you can work toward, not the floor you can count on.

Reason 4: Your Rewards Are Accruing but Not Paying Out Yet

Some cards accrue rewards continuously but only distribute them on a quarterly or annual schedule. The rewards are real and they will arrive, but they are not accessible now.

For agencies managing cash flow tightly, this distinction matters more than it sounds. A reward that posts to your account in December has less practical value than one that posts in January of the same year if you needed it to offset a billing cycle in March. Deferred rewards cannot be applied against current expenses, cannot be withdrawn to cover payroll, and cannot be used to reduce a balance that's accruing interest.

The cash flow illusion: A card paying 2% annually on $600k in ad spend generates $12,000 in rewards. That looks meaningful. But if those rewards post once per year and you're managing monthly cash cycles, you're essentially extending an interest-free loan to your card issuer for up to 11 months on money that was supposed to be working for you.

Check your card's reward payout schedule in the terms. Look for language about "statement credit posting," "annual reward distribution," or "quarterly payout." If the schedule isn't monthly, factor the delay into your actual expected value.

Reason 5: Non-Ad Spend on the Same Card Is Diluting Your Rate

If you use the same card for both ad spend and general business expenses, your total rewards will always reflect a blended rate across all spend categories, not just the ad spend rate.

The math is simple and the effect is larger than most people expect.

Spend Mix |

Ad Spend Rate |

General Spend Rate |

Blended Rate |

|---|---|---|---|

100% ad spend |

3% |

1% |

3.0% |

75% ad spend |

3% |

1% |

2.5% |

50% ad spend |

3% |

1% |

2.0% |

25% ad spend |

3% |

1% |

1.5% |

A card earning 3% on ad spend and 1% on everything else, used for an even mix of ad spend and general expenses, delivers a blended 2%. Most users mentally anchor to the headline ad spend rate and compare it against their total rewards statement without accounting for the non-qualifying spend pulling the average down.

The fix is straightforward: dedicate a separate card exclusively to ad spend and use a different card for everything else. This keeps your ad spend rewards clean and makes it easy to verify you're actually earning the rate you expect. Running high ad spend volumes on Google Ads and other platforms makes this separation especially valuable.

Reason 6: You're Earning Points, Not Cash, and the Redemption Rate Is Lower

Points programs are not the same as cashback programs, even when they advertise equivalent rates. The difference shows up at redemption.

A card advertising "3x points on advertising" is not offering 3% cash back. It's offering 3 points per dollar. The cash value of those points depends entirely on how you redeem them, and the advertised cents-per-point value almost always assumes optimal redemption: business class flights, hotel transfers, or specific travel portals.

Here's what that looks like in practice:

-

Optimal redemption (transfer partners, premium travel): 1.5-2 cents per point, delivering an effective 4.5-6% cash equivalent

-

Travel portal redemption: typically 1-1.25 cents per point, delivering 3-3.75% effective value

-

Statement credit redemption: often 0.6-1 cent per point, delivering 1.8-3% effective value

-

Cash back redemption: often the lowest option, sometimes as low as 0.5-0.6 cents per point

If you're redeeming for statement credits or cash back rather than booking premium travel, your effective rate on a "3x points" card may be closer to 1.5-2% than 3%. The advertised rate assumed you'd fly business class, not apply rewards to your monthly statement.

The honest question to ask: What do you actually do with rewards? If the answer is "apply them to my bill" or "transfer to cash," price the card at its cash redemption rate, not its travel redemption rate. That's the number that reflects your real-world return.

What to Actually Look for in an Ad Spend Rewards Card

Once you understand the six mechanisms above, evaluating a rewards card becomes a much simpler exercise. You're looking for three things:

1. No spend caps

The rate should apply to every dollar, not just the first $X per year. If a card caps its bonus category, the effective rate for high-volume ad spenders is always lower than the headline. Ask: "Does this rate apply to all spend, or is there a monthly or annual cap?"

2. No conditions required to earn the rate

The rate should be the base rate, not a conditional ceiling. If earning the advertised rate requires enrollment in additional programs, pre-funding accounts, or hitting behavioral thresholds, the actual rate for a standard user is lower. Ask: "What do I earn if I just use the card normally?"

3. Cash, not points

Statement credits and points introduce redemption variables that reduce effective value for most users. A straightforward cash rate is worth exactly what it says. Ask: "Is this a cash reward, or a points rate that assumes optimal redemption?"

A card that satisfies all three criteria delivers a predictable, consistent return without requiring you to manage conditions or optimize redemptions. Opal's 1% uncapped cashback is built on this model: a flat rate that applies to all ad spend, paid as cash, with no caps and no enrollment requirements. It's a lower headline number than some competitors advertise. It's also a number you can actually count on.

For high-volume ad spenders, predictability compounds. Knowing exactly what you'll earn every month is worth more than chasing a headline rate that most users never actually hit.

Frequently Asked Questions

Why is my cashback lower than expected?

The most common reasons are spend caps (your card stops paying the bonus rate after a certain threshold), merchant category code mismatches (your ad spend doesn't qualify as the bonus category), or conditional rates (the headline rate requires enrollment or specific behaviors you haven't completed). Check your card's terms for all three before assuming it's a calculation error.

Do Google and Meta qualify for advertising bonus categories?

Not always. Whether Google, Meta, TikTok, or other ad platforms qualify as "advertising" depends on the merchant category code assigned to each platform by the card network. Some platforms code as "computer services" or "online services" rather than "advertising," which means they earn the base rate even on cards that offer elevated rewards for advertising spend. Verify with your card issuer which MCCs qualify.

What's the difference between cashback and points for ad spend?

Cashback is a fixed percentage returned as cash or a statement credit with a known value. Points have a variable redemption value that depends on how you use them. A "3x points" card may deliver anywhere from 1.5% to 6% effective cash value depending on whether you redeem for cash, statement credits, or premium travel. For ad spend, where the goal is usually to offset costs rather than book flights, cash rewards are simpler to evaluate.

What does "uncapped cashback on advertising" actually mean?

It means the reward rate applies to every dollar of qualifying spend with no annual or monthly maximum. Most standard business cards cap bonus-category rewards at a threshold (often $50k-$150k per year). An uncapped card pays the same rate on dollar one and dollar one million. For agencies or media buyers running significant monthly ad budgets, uncapped rewards are the only way to ensure the advertised rate reflects what you actually earn.

How do I calculate my effective cashback rate?

Divide your total rewards received over a period by your total spend during the same period. If you received $1,800 in rewards on $120,000 in total card spend, your effective rate is 1.5%. Compare that to the headline rate you were advertised to identify the gap. Then use the six reasons in this post to determine which mechanism is responsible.