Meta Ads Billing Threshold Explained: Why Your Card Gets Declined and How to Fix It

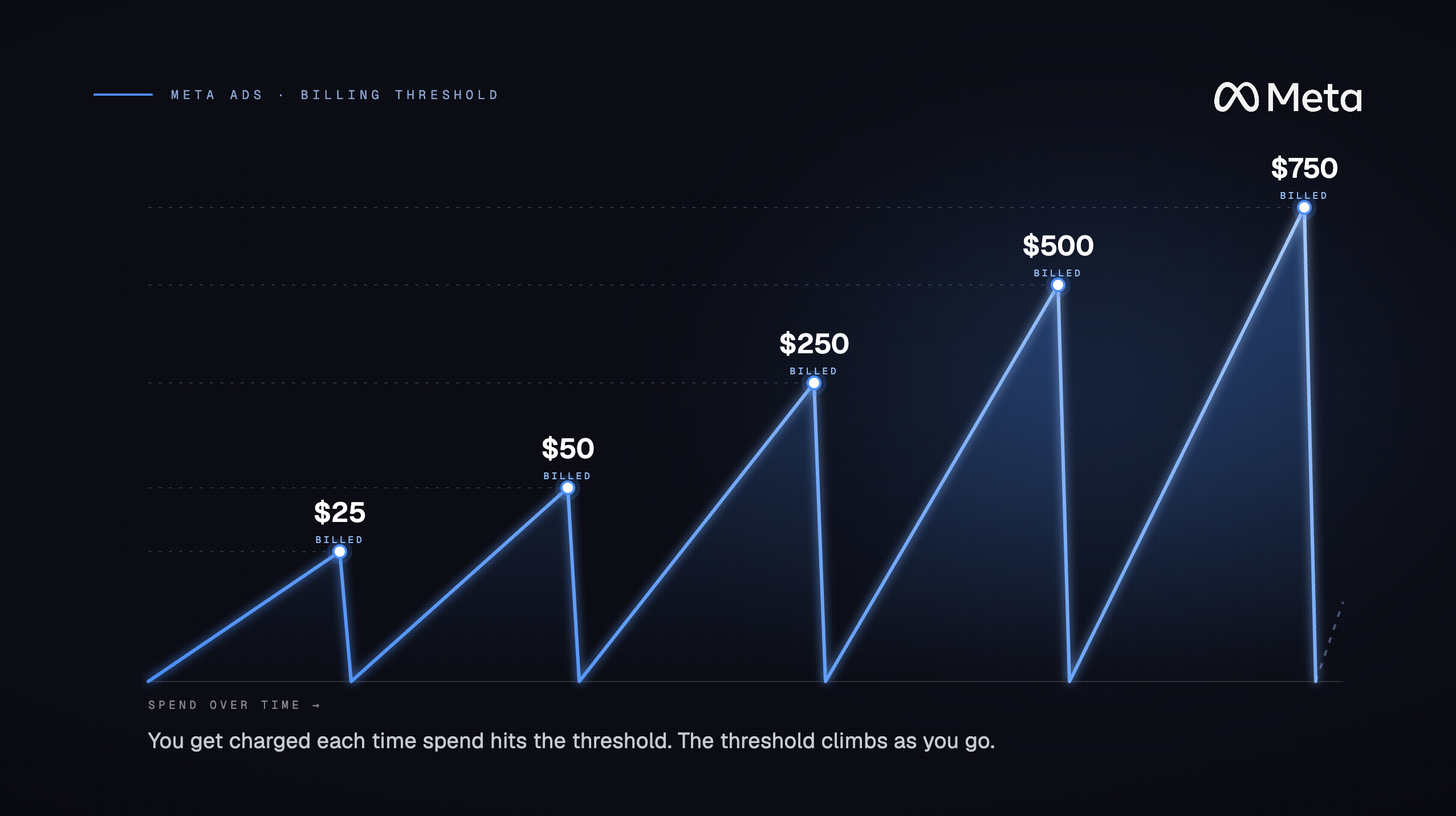

A billing threshold is the amount Meta charges to your card before your monthly billing date. Once your spend hits that threshold, Meta bills immediately and resets the counter, which can trigger multiple charges in a single day.

That one sentence is the source of more campaign pauses, confused finance teams, and declined cards than almost anything else in paid media. Most advertisers don't understand how Meta's billing system actually works until a campaign goes dark at the worst possible moment.

This post covers the full mechanics: how thresholds are set, why they cause declines at scale, the specific numbers involved, and the structural fixes that prevent the problem from recurring.

TL;DR:

Meta bills you when your ad spend reaches a billing threshold or when your monthly billing date arrives, whichever comes first. New accounts often start with a low threshold, and thresholds can rise with successful payment history. At higher daily spend, a low threshold can mean multiple charges per day against the same card, increasing the risk of declines, fraud flags, or campaign pauses. The fix is to isolate spend with one dedicated virtual card per ad account and use a card program with enough capacity for high-volume ad billing.

How Meta's Billing Threshold System Actually Works

Meta uses two triggers to charge your card, whichever comes first:

-

Your billing threshold is reached. Spend hits the set amount, charge fires immediately, balance resets to $0.

-

Your monthly billing date arrives. Whatever balance remains gets charged, even if you haven't hit the threshold.

Most advertisers assume Meta bills monthly like a utility. It doesn't. The threshold model means charges happen in real time, continuously, as your campaigns spend.

The Trust-Based Progression

Meta's billing threshold system is designed around payment trust. New accounts start low because Meta has no payment history with you. Every successful charge builds that history, and the threshold rises automatically as a result.

A typical threshold progression may look like this, although exact amounts and timing can vary by account, currency, region, payment history, and Meta relationship:

Stage |

Typical Threshold |

What It Takes |

|---|---|---|

New account |

Low starting threshold |

Verified payment method |

Early stage |

Gradual threshold increases |

Successful payments with no declines |

Established account |

Higher threshold range |

Consistent spend and clean payment history |

High-volume account |

Higher account-specific threshold |

Strong payment record and stable billing behavior |

Managed account |

Custom billing options may be available |

Meta account team or managed relationship |

Moving from a low starting threshold to a higher threshold usually takes consistent payment history over time. There is no guaranteed shortcut, and the timing can vary by account.

Meta's official help documentation confirms the threshold rises automatically as you make successful payments, with no manual override available.

What Can Lower or Disrupt Your Threshold

A few issues can slow down threshold increases, reduce billing trust, or create account-level billing problems:

-

A missed or failed payment. One decline can damage billing trust and may slow future threshold increases.

-

A new ad account. Each new ad account may start with its own low threshold, even if your business has spend history elsewhere.

-

A policy flag or account restriction. Account reviews or restrictions can affect billing behavior and payment reliability.

This is why agencies often run into threshold issues. Every new client account may have its own billing history, threshold progression, and payment risk. The system is mechanical, but the operational impact is real.

Why Thresholds Cause Card Declines

What is a Meta billing threshold? A Meta billing threshold is the cumulative spend amount that triggers an automatic charge to your payment method. Meta charges your card every time your ad spend reaches this amount, then resets the counter. This is separate from your monthly billing date, which triggers a charge for any remaining balance regardless of threshold status. New accounts start at $25. Thresholds rise automatically with successful payment history and can reach $5,000+ for established high-volume accounts.

Here is the mechanics problem that catches most high-volume advertisers off guard.

Meta doesn't bill against your monthly budget. It bills against your threshold, in real time, every time your cumulative spend crosses that line. At low spend volumes, this is invisible. At scale, it becomes a card management crisis.

The Math at Scale

Say you are running $50,000 in daily ad spend across a single ad account with a $2,500 billing threshold. That can create around 20 separate charges in one day. Each charge is a real authorization request against your payment method.

If that payment method has a $50,000 credit limit, you are not just managing the monthly budget. You are managing available balance, authorization timing, settlement timing, and issuer risk controls. By the time enough threshold charges hit, the card may run out of available credit or trigger a fraud review. The next charge declines, and Meta can pause the campaign until the balance is cleared.

The cascade looks like this:

Threshold hit fires a charge

Card issuer declines (limit exhausted or fraud flag from rapid-fire charges)

Meta pauses the ad account immediately

Campaigns go dark, auction momentum is lost

Restarting campaigns means re-entering the learning phase

The auction momentum loss is the part people underestimate. Meta's algorithm builds performance data over time. A campaign pause doesn't just stop spend for a few hours. It can set your ROAS back days or weeks while the algorithm relearns. This is why choosing the right card for Meta ad spend is a performance decision, not just a finance one.

Why Credit Card Limits Compound the Problem

Why does Meta charge my card multiple times a day? Meta charges your card every time your cumulative ad spend reaches your billing threshold, not once per day or once per month. If your threshold is $500 and you spend $5,000 in a day, Meta will attempt 10 separate charges against your payment method. Each charge is a real authorization request. If any one of them fails, your campaigns pause immediately until the balance is cleared.

A credit card has a hard limit. Once you hit it, nothing clears. At $50K daily spend with a $2,500 threshold, you need a card that can absorb 20 successful charges totaling $50,000 in a single day, and then do it again the next day. Most credit cards aren't built for that volume of rapid-fire authorizations even if the stated limit appears sufficient, because the available balance depletes faster than the card issuer can process settlements.

A credit card has a hard limit. Once you hit it, nothing clears. At $50K daily spend with a $2,500 threshold, you need a card that can absorb 20 successful charges totaling $50,000 in a single day, and then do it again the next day. Most credit cards aren't built for that volume of rapid-fire authorizations even if the stated limit appears sufficient, because the available balance depletes faster than the card issuer can process settlements.

How to Raise Your Meta Billing Threshold

The honest answer: you cannot force Meta to raise your threshold. The system is automated and trust-based. What you can do is build the payment history that triggers automatic increases, and avoid the behaviors that reset it.

What Actually Works

-

Pay on time, every time. This is the only reliable lever. Every successful threshold charge is a data point in Meta's trust model. Consistent payments over 2-3 months move you from $25 to $250. Six months of clean history gets you to $2,500+.

-

Keep your payment method current. Expired cards cause declines that look like missed payments to Meta's system. Audit your payment methods before they expire.

-

Don't dispute charges unnecessarily. Chargebacks and disputes signal payment unreliability. If there's a legitimate billing error, contact Meta Business Support directly before initiating a dispute with your bank.

-

Contact Meta Business Support with documentation. If you have a managed account relationship or a dedicated account rep, you can request a manual threshold review. Come prepared with 3-6 months of spend history showing consistent payment. This doesn't guarantee an increase, but it's the only path to accelerating the timeline. You can reach Meta's support team through Meta Business Help Center.

What Doesn't Work

-

Asking without documentation. Meta's support team cannot override the automated system without evidence of payment history.

-

Switching payment methods repeatedly. Every new card starts a fresh trust relationship. Frequent switches reset your progress and can flag the account for review.

-

Adding prepaid cards or gift cards. These often fail during rapid-fire threshold charges and create exactly the decline history you're trying to avoid.

The realistic timeline: A brand-new ad account spending $500/day will reach a $500 threshold in roughly 6-8 weeks with zero payment failures. Getting to $2,500 takes 4-6 months. Enterprise thresholds ($750K+) require a formal managed account relationship with a Meta account team.

The Virtual Card Fix

The root cause of the threshold collision problem at agencies isn't the threshold itself. It's stacking multiple ad accounts against a single payment method.

When you run 20 client accounts on one card, you're running 20 independent threshold clocks against a single payment ceiling. Each account has its own threshold. Each account fires charges independently. The card doesn't know it's servicing 20 separate billing relationships. It just sees an avalanche of charges and eventually runs out of available balance.

The fix is structural: one dedicated virtual card per ad account.

Here's why this works. Each virtual card has its own billing relationship with Meta. Its own threshold progression. Its own charge history. When Account A hits its $500 threshold, that charge fires against Card A's available balance only. Account B's threshold hit fires against Card B. The charges are isolated. No single card absorbs the full combined spend of your entire portfolio.

This also means each card builds its own threshold history independently. A new client account on its own card starts at $25 and progresses to $2,500 on its own timeline, without affecting or being affected by your other accounts.

How Agencies Implement This

The practical approach for a multi-client agency managing ad spend:

Issue one virtual card per client ad account

Set per-card spend controls sized to that client's actual monthly budget

Each card's threshold progresses independently based on that account's payment history

A decline on one card affects only that account, not your entire portfolio

Opal issues unlimited virtual cards per account with per-card spend controls, sized to actual managed spend volume. It is a charge card, not a credit card, which means no revolving balance and no interest charges because the balance is paid in full each billing cycle.

The agency running 20 client accounts on one legacy business card isn't just risking declines. It's building 20 threshold clocks against one payment ceiling, creating a structural failure that gets worse as the book of business grows. For a deeper look at how agencies should structure card assignments across clients and platforms, see how agencies structure ad spend by client.

Where Charge Cards Outperform Credit Cards for Meta Billing

Virtual cards solve the isolation problem. But the underlying card type still matters because it determines how much capacity you have when threshold charges hit quickly.

The structural difference is simple: a credit card usually has a fixed revolving limit, while a charge card is typically designed to be paid in full each cycle and may offer more flexible spend capacity based on underwriting, account history, and business volume.

When Meta fires multiple threshold charges against a credit card in one day, each charge reduces available credit. Once the limit is exhausted, the next charge can decline. A charge card can reduce that hard-limit risk when it is sized for actual managed spend and the account remains in good standing.

Here's how the two card types compare across the scenarios that matter for Meta billing:

Scenario |

Credit Card |

Charge Card |

|---|---|---|

Daily threshold hits |

Risk of hard limit exhaustion |

Clears without interruption |

Multiple accounts on one card |

Shared ceiling, compounding risk |

Same risk: use virtual cards |

Threshold reset after missed payment |

Balance carries, interest accrues |

Full balance due, no interest |

Campaign continuity |

At risk during spend spikes |

Strong with proper cash flow |

The "multiple accounts on one card" row is the same for both card types. The virtual card fix applies regardless of whether the underlying card is a credit card or a charge card. But the daily threshold hit row is where charge cards create a meaningful structural advantage for high-volume campaigns.

Is Opal a credit card? No. Opal is a charge card. There is no revolving balance, no interest charges, and no credit utilization impact. The full balance is due each billing cycle. Opal extends credit directly to your agency based on managed spend volume, with limits up to $10M, no personal guarantee, and no hard credit check required.

Frequently Asked Questions

What is the Meta Ads billing threshold?

The Meta Ads billing threshold is the cumulative spend amount that triggers an automatic charge to your payment method. Once your ad spend reaches this amount, Meta charges your card immediately and resets the counter to zero. Charges also fire on your monthly billing date for any remaining balance below the threshold. New accounts start at $25. Thresholds increase automatically with a consistent on-time payment history.

Why did Meta charge my card multiple times today?

Meta charged your card multiple times because your ad spend crossed your billing threshold more than once in a single day. If your threshold is $500 and you spent $2,000, Meta attempted four separate charges. This is normal behavior, not an error. If any single charge failed, your campaigns would have paused until the balance was cleared.

How do I raise my Meta billing threshold?

You cannot manually request a threshold increase and expect it to work without documentation. The system is automated. The only reliable method is consistent on-time payment history over 2-6 months. If you have a managed account relationship with a Meta account rep, you can request a manual review with spend history documentation. Switching payment methods, disputing charges, or adding prepaid cards will slow or reverse your progress.

What happens when my card is declined on Meta Ads?

When a threshold charge is declined, Meta pauses your ad campaigns immediately. The campaigns remain paused until you clear the outstanding balance, either by paying manually through Billing settings or by updating your payment method. Once the balance clears, campaigns restart, but your auction momentum and algorithm learning may be partially reset depending on how long the pause lasted.

How do I stop Meta from declining my card?

Three approaches work in combination: raise your threshold over time through clean payment history, use a card with sufficient capacity to absorb your daily threshold charge volume, and use one dedicated virtual card per ad account so no single card absorbs the full spend of multiple accounts simultaneously.

Does using a virtual card help with Meta billing thresholds?

Yes, significantly for agencies and multi-account operators. Each virtual card has its own billing relationship with Meta, its own threshold progression, and its own available balance. Isolating each ad account to its own virtual card means a decline on one account doesn't affect any other. It also means each account builds its own threshold history independently.

What is the starting billing threshold for a new Meta Ads account?

New Meta Ads accounts often start with a low billing threshold, but the exact amount can vary by account, currency, region, payment method, and account history. As payments are completed successfully, Meta may increase the threshold over time. Larger or managed accounts may have access to higher thresholds or different billing arrangements through a Meta account team.

Is Opal a credit card?

No. Opal is a charge card. There is no revolving balance and no interest because the full balance is due each billing cycle. Opal offers unlimited virtual cards, per-card spend controls, 1% uncapped cashback on major ad platforms, and limits up to $10M based on managed spend volume.

Is Opal a credit card?

No. Opal is a charge card. There is no revolving balance, no interest, and no credit utilization impact. The balance is due in full each billing cycle. Opal extends credit directly to your agency based on managed spend volume, with limits up to $10M, no personal guarantee required, and no hard credit check to get started.