How to Turn Ad Spend Into a Revenue Line for Your Agency

Most agencies track ROAS, CPA, and CPM down to two decimal places. Very few track what their card returns on the same spend.

That gap is costing them real money every month.

An agency running $500,000 in monthly client ad spend is putting $6 million through a card every year. At 1% cashback with no cap, that is $60,000 returned annually. No new clients. No renegotiated retainers. No additional headcount. The spend was already happening. The only question is whether the card it runs through converts it into revenue or lets it pass through as a zero-return transaction.

Most cards let it pass through. That is the problem this post fixes.

TL;DR

At 1% uncapped cashback, a $500K/month agency can generate $60K/year in additional margin on spend it was already managing. The structural setup is simple: use a card built for high-volume ad spend, assign one virtual card per client or ad account, and understand how platform billing events interact with card capacity. This post walks through the math, the card architecture, and the setup.

The Math First

Before anything else, run this calculation against your own number.

Take your total monthly managed ad spend across all clients. Multiply by 0.01. That is your monthly cashback at 1%. Multiply by 12 for the annual figure.

Here is what that looks like across common agency spend levels:

Monthly Managed Ad Spend |

Monthly Cashback |

Annual Cashback |

|---|---|---|

$100,000 |

$1,000 |

$12,000 |

$200,000 |

$2,000 |

$24,000 |

$300,000 |

$3,000 |

$36,000 |

$500,000 |

$5,000 |

$60,000 |

$1,000,000 |

$10,000 |

$120,000 |

These are not projections. They are the direct result of applying a 1% cashback rate to spend agencies are already running for clients.

The critical point: this cashback can come from spend the agency is already managing. Opal extends credit directly to your agency, sized to managed spend volume. You run approved client budgets through the card, and cashback accrues to the agency according to your card terms and client agreements.

At $200K/month, that is $24,000/year flowing directly to margin. At $500K/month, it is $60,000. That is a full-time junior hire, a meaningful growth investment, or pure bottom-line improvement. And it compounds: every month you are not capturing it is a month of cashback permanently forfeited. It does not roll over.

For a deeper look at how this cashback compounds over time and how to present it to agency ownership, see how digital agencies earn cashback on ad spend.

Why Most Agencies Are Earning Zero

The agencies not capturing this cashback are not making a strategic decision. They inherited a card. The card came with the business checking account, or was chosen for a conference trip in 2019, or is whatever the founder put on file when they first loaded a Google Ads campaign.

Nobody evaluated it as a financial instrument for ad spend at scale. Because the question never came up.

The Three Ways Generic Cards Fail Agencies

Generic business cards fail agencies on ad spend in one of three predictable ways:

-

Reward caps. Most standard business cards cap cashback at a fixed annual spend threshold, often $50,000 to $150,000. An agency running $200K/month hits that ceiling in the first month of January and earns nothing for the remaining eleven months.

-

Points instead of cash. Points programs add a conversion layer between spending and value. A point might be worth $0.01 under one redemption and $0.015 under another. Cash is cash. Points are a discount program with a redemption step.

-

Ad spend excluded from bonus categories. Some cards offer elevated rewards on travel and dining but explicitly exclude digital advertising. The category that represents the majority of agency spend gets the worst rate on the card.

The result: agencies running $500K/month in client ad spend are often earning $0 in cashback, or close to it. The spend passes through as a zero-return transaction, month after month.

For a detailed breakdown of how reward caps quietly eliminate cashback at scale, see cashback on ad spend: the hidden cost of card caps.

Charge Card vs. Credit Card: Why the Card Type Matters

Most people treat "charge card" and "credit card" as interchangeable terms. For agencies running high ad spend, they are not. The distinction is structural, and it directly affects whether your cashback program actually works at scale.

How a Credit Card Works at High Ad Spend

A credit card extends a revolving line of credit up to a fixed limit. You spend, you carry a balance, you pay interest if you do not pay in full. The limit is set at account opening based on a credit assessment, and it moves slowly if it moves at all.

The problem at agency scale: ad spend is not evenly distributed. Meta's billing threshold system charges your card in unpredictable increments, sometimes multiple times per day during high-spend periods. A credit card with a $25,000 limit can be exhausted in the first week of a $100K/month campaign. When the card hits its ceiling, Meta pauses delivery. Campaigns go dark. You spend hours on the phone with your bank asking for a temporary increase.

Repeated payment declines can create real performance issues. Campaigns may pause, delivery can be interrupted, and teams may lose time rebuilding momentum once payment issues are resolved. That is not just a billing inconvenience. It can become a performance problem.

How a Charge Card Works Differently

A charge card is designed to be paid in full each billing cycle rather than carried as revolving debt. Depending on the issuer, available spending capacity may be sized around business volume, repayment history, cash flow, and managed spend rather than a fixed credit line set once at account opening.

For agencies, this matters in three specific ways:

-

Limits sized around managed spend. Opal offers limits up to $10M based on managed spend volume, helping agencies support larger client budgets without relying on a traditional small-business card limit.

-

No revolving interest. Because the balance is paid in full each cycle, there is no revolving interest. That makes the cashback easier to treat as a true margin improvement.

-

More reliable platform billing. A card program with enough capacity and clean payment history can reduce the risk of declines on Meta, Google, and other ad platforms. Fewer payment issues means fewer campaign interruptions and less operational cleanup.

Key takeaway: A credit card with a $25K limit is a liability at $200K/month in ad spend. A charge card sized to your managed spend volume is infrastructure.

For a deeper look at how credit limits interact with ad platform scaling, see higher ad spend limits without a personal guarantee.

The Structural Setup: How to Actually Do This

The barrier to capturing this return is lower than most agencies assume. You do not need a new bank relationship, a months-long finance evaluation, or a CFO sign-off on a complex program. You need to replace a card number and set up the right architecture around it.

Step 1: One Virtual Card Per Client

Issue a dedicated virtual card for each client account. That card goes on file with every ad platform that client uses: Google, Meta, TikTok, LinkedIn, Snapchat, wherever their spend runs.

This is not just about organization. It is about cashback capture and risk isolation. A shared card across five clients means one decline can pause every client's campaigns simultaneously. A dedicated card per client means a problem on one account stays contained. It also means your reconciliation is automatic: every charge on a client's card is that client's spend, no sorting required.

Step 2: Match Card Limits to Spend Volume

Set a monthly spend limit on each card that matches the client's approved budget. This turns budget enforcement from a reactive process into a proactive one. The card declines when the limit is hit, not after.

For Meta specifically, understand how threshold billing works. Meta may charge your card whenever cumulative spend reaches your billing threshold, as well as on your monthly billing date for any remaining balance. Threshold amounts and timing vary by account, currency, region, payment history, and account status. At higher spend volumes, that can mean multiple card charges in a month or even in a day. Your card capacity needs enough headroom for threshold charges, retries, verification holds, and timing gaps between authorizations and settlements.

The practical rule: your card limit per client should be at least 3x the highest expected single threshold charge, with room for retries and verification holds.

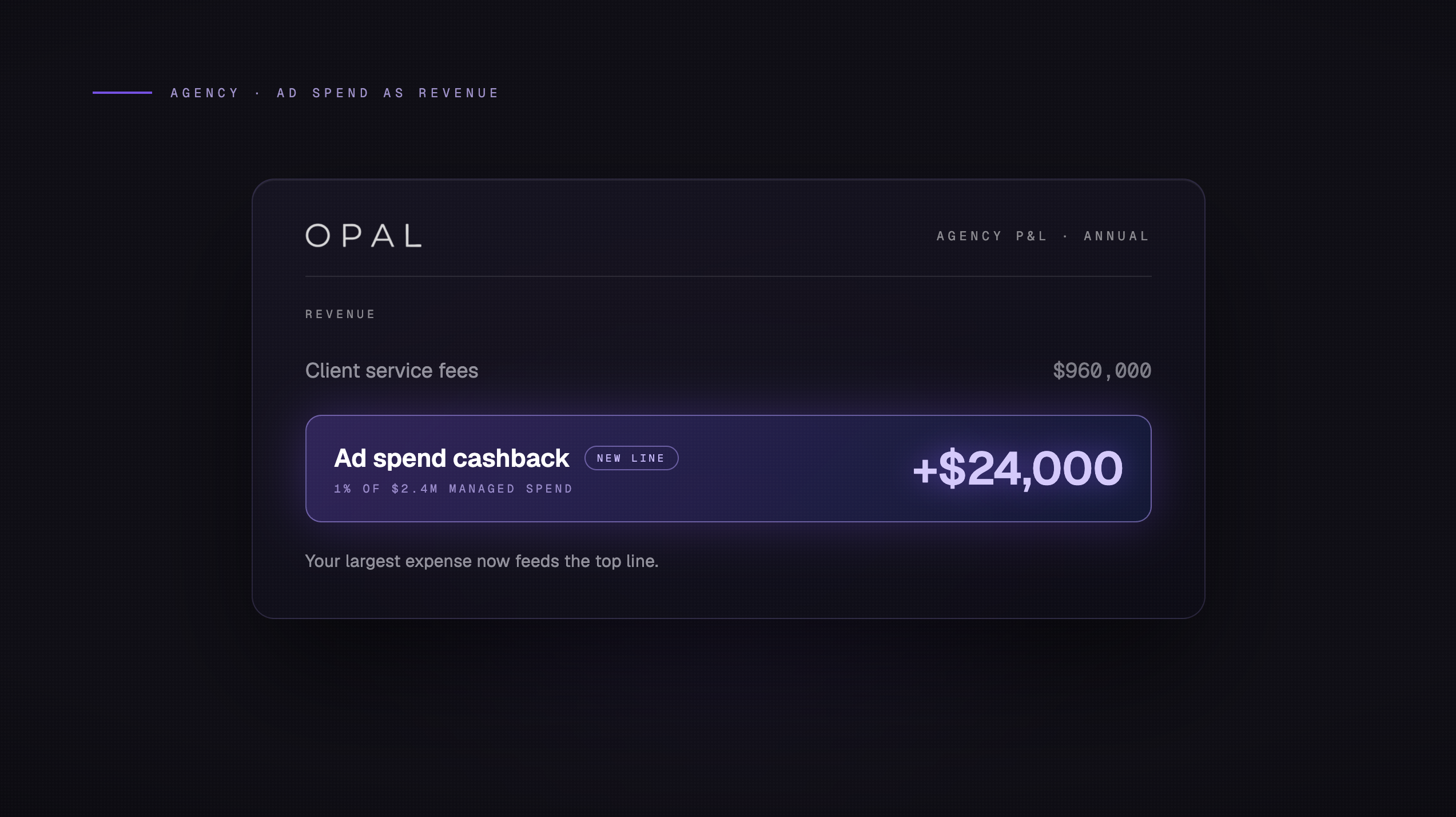

Step 3: Treat Cashback as a Line Item

Cashback earned on business card spend is typically recorded as either other income or a reduction in advertising expense. Both approaches are acceptable; the priority is consistency across reporting periods so the income appears cleanly in your P&L.

The framing that works best internally: present it as a margin improvement on every managed account. Every client generating ad spend is now generating passive cashback revenue for the agency, with no operational change required.

"Opal has transformed how we manage finances. The cashback alone has become a significant revenue stream. We're more profitable, more efficient, and our clients love the transparency." — Operations Lead, Outsmart Labs

For a detailed walkthrough of how cashback integrates into agency financial reporting and QuickBooks reconciliation, see how digital agencies earn cashback on ad spend.

What to Do With the Cashback

Cashback revenue is unrestricted cash. How you deploy it determines how much strategic leverage it creates.

The three most common uses agencies report:

-

Offset overhead. Software subscriptions, contractor costs, platform fees, and reporting tools that currently come out of margin can be partially or fully covered by cashback income. An agency earning $2,000/month in cashback can eliminate $24,000 in annual overhead without touching retainer revenue.

-

Improve net margin on retainer accounts. Most agency retainers are priced on a fixed monthly fee. Cashback adds a passive margin layer to every account that generates ad spend, without renegotiating pricing or reducing service quality.

-

Fund growth. At $500K/month in managed spend, $5,000/month in cashback is a meaningful growth budget: a new hire, a channel experiment, a tooling investment that would otherwise require justifying against existing margin.

The agencies winning on margin in 2026 are not just billing more. They are building passive revenue into the operational model.

There is also a competitive angle worth considering. An agency that earns 1% cashback on client ad spend has a structurally lower cost base than one that does not. Some agencies use this to price more competitively, absorb platform fees, or offer enhanced reporting at no additional cost. The cashback subsidizes the client relationship.

How Opal Is Built for This

Opal is a charge card built exclusively for agencies and brands running serious ad spend. It is the only card in this space designed around the multi-client agency use case from the ground up.

The core specs:

-

1% uncapped cashback on every dollar of ad spend across Google, Meta, TikTok, Snapchat, LinkedIn, Amazon, The Trade Desk, and others. No category caps. No annual ceiling.

-

Credit limits up to $10M, sized to your managed spend volume, not your personal credit history. No personal guarantee. No hard credit check.

-

Unlimited free virtual cards, issued instantly. One per client, one per platform, however you want to structure it.

-

No annual fee. No platform fee. No cancellation fee.

-

QuickBooks integration that automatically reconciles ad spend by client and card, eliminating the manual bookkeeping overhead that makes high-volume card programs operationally painful.

The application takes two to three minutes. Most agencies are live within a few days.

For a direct comparison of how Opal stacks up against the cards agencies most commonly use, see the best credit card for Facebook Ads, which includes a full breakdown of how Meta's billing threshold system interacts with different card architectures.

Your ad spend is already going out every month. The only question is whether it is coming back.

See what Opal returns on your current spend volume at opalspend.com.

Frequently Asked Questions

Does the agency earn cashback on client money it never touched?

Yes, if the agency is the cardholder and the spend is structured that way. Opal extends credit directly to the agency, and cashback accrues according to the agency's card terms. Agencies should make sure their client agreements clearly explain how ad spend, billing, and any card rewards are handled. This keeps the setup clean and avoids confusion around who owns the rewards.

Is cashback on ad spend taxable income?

Generally, the IRS treats cashback earned on business purchases as a reduction in the cost of those purchases rather than taxable income. This means your effective ad spend cost is reduced by the cashback amount for accounting purposes. Tax treatment can vary based on your business structure. Consult your accountant for guidance specific to your situation.

What happens when Meta moves a high-spend account to invoice billing?

Meta and Google sometimes move high-spend accounts off card billing and onto monthly invoice billing once spend volume crosses certain thresholds. When that happens, Opal's Ad Pay feature automatically detects those invoices from your inbox and lets you pay them with Opal credit or a connected card in one click, extending cash flow up to 55 days and earning 1% cashback on every dollar paid.

How quickly can an agency get set up?

The Opal application can take up to 10 minutes. No calls, no lengthy underwriting process, no hard credit check. Most agencies receive their virtual cards and are live on ad platforms within a few days. Switching a card on file at Google, Meta, or TikTok takes under five minutes per platform.

Does cashback apply across all ad platforms?

Yes. Opal's 1% cashback applies across every platform where your ad spend runs: Google, Meta, TikTok, Snapchat, LinkedIn, Amazon, Apple, The Trade Desk, and others. The rate is not category-specific or platform-specific. Every dollar charged to the card earns the same rate, regardless of where it goes.