Charge Card vs. Credit Card for High Ad Spend: What Actually Matters

The short answer: A charge card requires full payment each billing cycle and carries no revolving balance. A credit card lets you carry a balance and pay interest on it. For businesses running $50K or more per month in digital advertising, that structural difference has real consequences for cash flow, credit scores, and whether your campaigns stay live.

Executive Summary

Charge cards and credit cards are not interchangeable at high ad spend volumes. Charge cards typically require full payment each cycle, do not carry revolving balances, and may reduce the credit utilization issues that come with traditional credit cards. Credit cards offer float and flexibility but introduce interest costs, fixed limits, and utilization risk that can compound quickly at scale. For operators running $50K or more per month, the wrong choice can compress your credit profile, trigger declined transactions at peak spend, and quietly cost thousands in interest. This post breaks down the structural differences, where each product wins, and what to look for if you decide a charge card is the right tool for your ad operation.

The Core Structural Difference

A charge card is not a credit card. The distinction matters more than most operators realize until they hit a limit or a billing cycle problem.

The difference between a charge card and a credit card: A charge card requires you to pay your full balance at the end of each billing cycle. There is no option to carry a balance forward, and there is no interest rate because there is no revolving debt. A credit card lets you pay a minimum amount and carry the rest forward, accruing interest on the unpaid balance.

That single structural difference cascades into several downstream effects:

Feature |

Charge Card |

Credit Card |

|---|---|---|

Revolving balance |

No |

Yes |

Interest charges |

None |

15-29% APR typical |

Preset spending limit |

Often none (or very high) |

Fixed credit limit |

Credit utilization impact |

None |

Yes, affects credit score |

Payment terms |

Full balance due each cycle |

Minimum payment option |

Best for |

High, predictable business spend |

Flexible personal or business spend |

Payment Terms and Billing Cycles

Charge cards typically bill on a fixed monthly cycle. You spend throughout the month, and the full balance is debited automatically at the end of the period. Some charge cards offer net-30 or net-60 terms for businesses, which extends the window between spend and payment.

Credit cards operate differently. Your statement closes on a specific date, your minimum payment is due roughly 21 days later, and the remaining balance rolls forward with interest. For low-volume spending, this flexibility is useful. For high-volume ad spend, it creates a debt trap most operators do not intend to fall into.

No Preset Spending Limit

Many charge cards do not work like traditional credit cards with a single fixed revolving credit line. Instead, approval can depend on underwriting, account history, repayment behavior, and real time risk checks. For high spend operators, the practical advantage is that a well designed charge card can be sized around actual business spend rather than a generic small business credit limit.

Credit cards have a fixed limit. Once you hit it, transactions decline. At $50K or more per month in ad spend, hitting that ceiling mid-campaign is not a theoretical risk. It is a recurring operational problem.

Why the Distinction Matters at High Ad Spend Volumes

Most financial content about charge cards vs. credit cards is written for consumers making $2,000 in monthly purchases. The decision changes once you are running $50K, $200K, or $500K per month through a card.

At that point, three problems start showing up.

Cash Flow Timing

Ad platforms charge your card in real time. Google, Meta, TikTok, and other ad platforms often charge based on thresholds, top ups, invoice settings, or spend activity. Those billing events rarely align cleanly with your client invoicing or revenue cycle.

A credit card lets you defer payment and manage that gap with float. A charge card requires you to pay the full balance each cycle, which means your cash flow needs to support the full spend amount without a buffer.

The tradeoff is real: charge cards eliminate interest costs but require stronger cash flow discipline. Credit cards provide a float buffer but introduce interest risk if balances are not cleared.

Credit Utilization at Scale

This is the most underestimated problem for high-volume ad operators using credit cards.

Credit utilization is the ratio of your current balance to your total credit limit. If you have a $100K credit limit and you are running $80K in ad spend, your utilization is 80%. Credit scoring models treat anything above 30% as a negative signal. Above 50%, the damage to your score is significant.

At $50K or more per month, a typical business credit card limit is not large enough to avoid high utilization unless you pay mid-cycle. Many operators do not realize their credit score is being compressed every month by their own ad spend.

Charge cards generally do not create the same revolving utilization ratio as credit cards because balances are paid in full rather than carried month to month. Depending on the issuer and reporting practices, this can reduce the risk that high ad spend compresses a credit score through utilization alone. Payment history still matters, and missed payments can create credit risk.

Statement Cycles vs. Billing Cycles

Ad platforms set their own billing thresholds, which often do not align with your card's statement cycle. Meta, for example, charges your card every time you hit a billing threshold (which can be daily at high spend), not once per month.

On a credit card with a $50K limit, a single day of heavy Meta spend can trigger multiple charges that collectively push you toward or over your limit before your statement even closes. On a charge card with higher or more flexible spend capacity, those same charges are less likely to hit a hard ceiling, assuming the account is in good standing and spend is within approved parameters.

Where Charge Cards Win

For businesses running significant ad budgets, charge cards have structural advantages that credit cards cannot replicate.

-

More flexible spend capacity. Many charge cards can scale with your actual spend patterns rather than relying on a fixed revolving credit limit set at account opening.

-

Less utilization pressure. Because charge cards generally do not create the same revolving utilization ratio as credit cards, high ad spend is less likely to compress your credit profile through utilization alone.

-

Built for business cash flow patterns. Charge cards assume you will pay in full each cycle, which aligns with how well-run businesses should operate. They are not designed around the possibility of revolving debt.

-

Rewards on volume. Charge cards built for business often offer flat-rate cashback on all spend, which at $100K per month means meaningful returns. A 1% cashback rate on $1.2M in annual ad spend generates $12,000 per year.

-

Operational controls. Business charge cards typically offer per-card spending limits, real-time transaction visibility, and virtual card issuance. These features matter when you are managing multiple campaigns, clients, or platforms simultaneously.

Opal, for example, is a charge card built specifically for ad spend. It offers 1% uncapped cashback across major ad platforms like Google, Meta, and TikTok, with limits up to $10M sized around managed spend volume. It is not a credit card and does not carry a revolving balance.

Is Opal a credit card? No. Opal is a charge card. It does not carry a revolving balance, does not charge interest, and does not report credit utilization. The full balance is paid each billing cycle.

Where Credit Cards Win

Credit cards are not the wrong tool in every situation. There are genuine advantages worth acknowledging.

-

Float. A credit card lets you spend now and pay later, sometimes 30-60 days after a purchase. For businesses with tight cash flow or unpredictable revenue timing, this buffer has real operational value.

-

Wider acceptance. Credit cards are accepted virtually everywhere. Some smaller vendors, international platforms, or niche ad networks may be more familiar with traditional credit cards, especially when a newer business card program is involved.

-

Lower barrier to entry. Getting approved for a business credit card is generally easier than qualifying for a high-limit charge card. If you are earlier in your business lifecycle, a credit card may be accessible when a charge card is not.

-

Rewards flexibility. Many consumer and small business credit cards offer tiered rewards: higher cashback on travel, dining, or specific categories. If your spend is diversified across many categories, a credit card rewards structure may outperform a flat-rate charge card.

-

Purchase protection and benefits. Consumer-grade credit cards often include extended warranties, purchase protection, and travel insurance. These benefits are less common on business charge cards.

The honest summary: credit cards are a better fit for lower-volume, diversified, or cash-flow-constrained operations. They become a liability at high ad spend volumes where utilization, interest, and hard limits create compounding problems.

What the wrong card can cost you at scale

The financial impact of using a credit card for high ad spend is not always obvious on the surface. It shows up in three places most operators do not track closely.

Interest on Revolving Balances

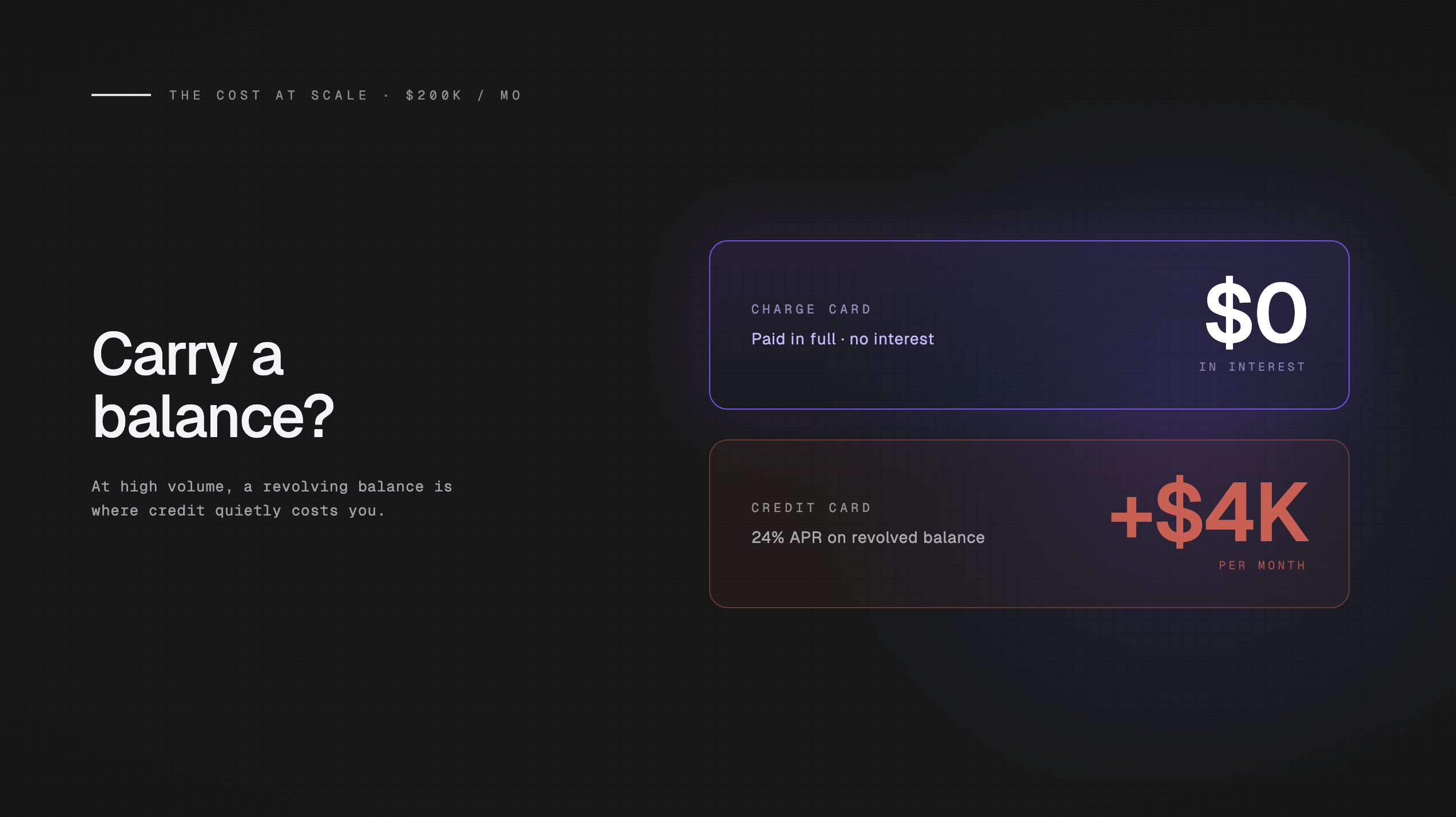

Business credit cards carry APRs typically ranging from 18% to 29%. If you run $100K in ad spend per month and carry even 20% of that balance forward, that is a $20K revolving balance. At an 18% to 29% APR, the monthly interest cost would be roughly $300 to $483 before accounting for compounding, fees, or additional carried balances. Over a year, that can become thousands of dollars in financing cost on top of the ad spend itself.

Most operators do not intend to carry a balance. But cash flow gaps happen. A slow client payment, a surprise expense, or a budget spike can push you into revolving territory quickly.

With a charge card, this cost is structurally zero. There is no APR because there is no revolving balance.

Credit Score Compression

High utilization on a business credit card can suppress your credit score by 50 to 100 points or more, depending on your baseline and the severity of utilization. A compressed credit score affects your ability to secure other financing: a business line of credit, a lease, or a loan.

The damage is particularly frustrating because it is self-inflicted by your own revenue-generating activity. You are running campaigns, generating results, and simultaneously weakening your credit profile.

Declined Transactions at Peak Spend

Hard credit limits on credit cards create a specific operational risk for ad buyers: declined transactions during high-spend periods.

Black Friday, Q4 holiday campaigns, product launch windows. These are exactly the moments when ad spend spikes. They are also exactly when a fixed credit limit is most likely to be exhausted. A declined card mid-campaign means paused ads, missed impressions, and potential loss of auction momentum that can take days to rebuild. The full cost of a declined ad payment matters, once campaigns pause, performance can take time to recover.

Which is better for high ad spend: a charge card or a credit card? For businesses running $50K or more per month in digital advertising, a charge card is structurally better. It eliminates credit utilization risk, has no preset spending limit to block peak-period transactions, and carries no interest cost. The tradeoff is that it requires stronger cash flow discipline since balances must be paid in full each cycle.

What to Look for in a Charge Card Built for Ad Spend

Not all charge cards are designed for advertising operations. A general-purpose business charge card may lack the features that make it practical for media buyers and agencies. Here is what actually matters.

Autopay Integration

The full-balance payment requirement of a charge card only works smoothly if payment is automated. Look for a card that supports autopay from a linked business bank account, with clear advance notice before each debit. Manual payment management at high spend volumes introduces unnecessary risk of missed payments and late fees.

Real-Time Spend Visibility

Ad spend moves fast. You need to see transactions as they post, not 24-48 hours later. Real-time visibility lets you catch billing errors, monitor budget pacing across platforms, and identify unauthorized charges before they compound. For agencies, real-time ad spend visibility is also a client retention and new business tool, not just an operational one.

Per-Card Spending Controls

If you are managing spend across multiple clients, campaigns, or platforms, the ability to issue separate virtual cards with individual spending limits is operationally essential. Separating client ad budgets at the card level is the structural fix most agencies defer too long. It eliminates the need to reconcile a single card statement across dozens of line items and makes client billing significantly cleaner.

Rewards Calibrated to Ad Platforms

General business rewards programs often exclude or cap cashback on advertising purchases. Look for a card that explicitly includes ad platform spend in its rewards calculation and does not impose category caps that reduce your effective return at high volumes. A flat 1% uncapped cashback on $500K per month is worth $5,000. A tiered card that caps ad spend rewards at $10K per month in eligible purchases is worth far less. The math on cashback caps at scale shows how quickly the gap compounds annually.

Credit Limits Sized to Actual Spend

A charge card with a $25K limit is not meaningfully different from a credit card with a $25K limit for a business running $200K per month. Look for issuers that size limits to your actual managed spend volume, not to a conservative estimate of what a typical small business needs.

No Personal Guarantee

At scale, it is worth looking for a card that can be underwritten primarily on the business's financial profile rather than relying on the owner's personal credit or a personal guarantee. A personal guarantee means your personal assets are on the line if the business has a bad month. For high-volume ad operators, this is an unnecessary and avoidable risk.

Summary: Charge Card vs. Credit Card for High Ad Spend

The choice between a charge card and a credit card is not a matter of preference at high ad spend volumes. It is a structural decision with measurable financial consequences.

Consideration |

Charge Card |

Credit Card |

|---|---|---|

Spend limit risk |

Low, with flexible spend capacity |

High (fixed ceiling) |

Interest cost |

Lower utilization pressure |

18-29% APR on carried balances |

Credit score impact |

None (no utilization) |

High at elevated spend volumes |

Campaign continuity |

Stronger, assuming spend is within approved parameters |

At risk during spend spikes |

Cash flow requirement |

Full balance each cycle |

Minimum payment option |

Best fit |

$50K+ monthly ad spend |

Under $50K, diversified spend |

The bottom line: If you are running $50K or more per month in digital advertising, a charge card eliminates three structural problems that credit cards create at scale: utilization-driven credit score compression, interest on unintended revolving balances, and hard-limit transaction declines at peak spend. The requirement to pay in full each cycle is a constraint, but for a well-run operation, it is a constraint that enforces financial discipline rather than creating risk.

Credit cards remain the right tool for businesses with lower or more diversified spend, tighter cash flow, or earlier-stage operations where a charge card is not yet accessible.

Frequently Asked Questions

What is the difference between a charge card and a credit card?

A charge card requires you to pay your full balance at the end of each billing cycle. There is no revolving balance and no interest charged. A credit card allows you to carry a balance forward and pay interest on the unpaid amount. Charge cards typically have no preset spending limit; credit cards have a fixed credit limit.

Do charge cards affect your credit score?

Charge cards generally do not create the same revolving utilization ratio that credit cards do because balances are expected to be paid in full. Reporting practices vary by issuer, so payment history can still matter, but high spend on a charge card is less likely to create the same utilization pressure as high spend on a credit card.

Which is better for high ad spend: a charge card or a credit card?

For businesses running $50K or more per month in digital advertising, a charge card is structurally better. It can offer more flexible spend capacity, reduces utilization pressure compared with traditional credit cards, and carries no interest cost because balances are paid in full. The key requirement is that you have sufficient cash flow to pay the full balance each cycle.

Can a credit card limit cause campaign interruptions?

Yes. Credit cards have fixed limits. At high ad spend volumes, it is possible to exhaust your available credit mid-campaign, causing transactions to decline. This is a common operational problem for media buyers and agencies using personal or small business credit cards for large ad budgets.

Is Opal a credit card?

No. Opal is a charge card, not a credit card. It does not carry a revolving balance, does not charge interest, and does not report credit utilization. The full balance is paid each billing cycle. Opal is designed specifically for businesses with high monthly ad spend across platforms like Google, Meta, and TikTok.

What happens if I miss a payment on a charge card?

Unlike credit cards, charge cards do not have a minimum payment option. Missing a payment typically results in late fees, potential account suspension, and in some cases a negative mark on your business credit report. This is why autopay is strongly recommended for any business using a charge card for high-volume ad spend.

Do charge cards earn rewards?

Yes. Many business charge cards offer cashback or points on all purchases. Cards designed specifically for ad spend may offer flat-rate cashback with no category caps, which is more valuable than tiered rewards programs that limit returns on advertising purchases.