How E-Commerce Brands Are Turning Ad Spend Into a Revenue Line

You probably know your ROAS down to two decimal places. You know your CPA by audience segment, your return by creative, your cost per click by platform. If you are spending $200K a month on ads, you have optimized almost everything there is to optimize.

Almost.

There is one lever most e-commerce brands have never touched, because it never occurred to them that it was a lever at all: the card the spend runs through. A small number of brands have figured out that the infrastructure they use to pay for ads can generate a return of its own, completely separate from campaign performance. It does not require spending more. It does not require a new agency or a new strategy.

The brands doing this aren't spending more. They're just making their spend work twice.

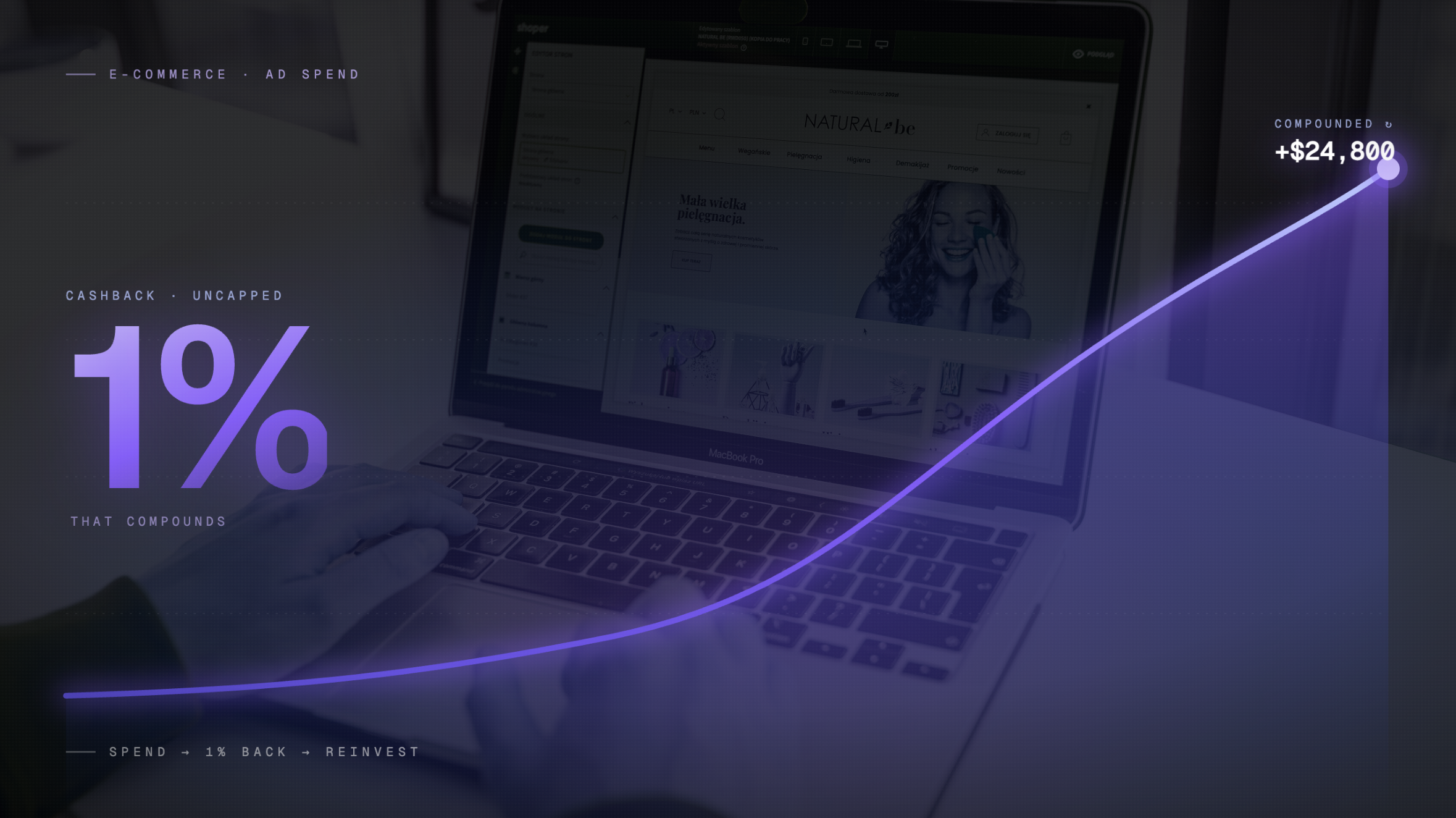

TL;DR: Most e-commerce brands optimize every part of their ad spend except the card it runs through. At 1% uncapped cashback, a brand spending $200K/month earns $24,000 back annually, automatically, regardless of ROAS. The setup takes minutes. Most brands are not doing it because they never thought of the card as a financial lever.

Why Ad Spend Is Still Treated as a Pure Cost Center

The default mental model for paid media is simple: money goes out, customers come in. The card is a utility. It is the thing you enter into the platform dashboard once, and then forget about until it declines.

Nobody sits down at a quarterly review and asks what their card is returning on $3M in annual ad spend. The question has never come up because it never seemed like the kind of question that had an answer. The card does not have a return. It is just how you pay.

That assumption is wrong. And it is costing brands real money every month.

The Math That Changes the Conversation

Before we get to a table, do the math for your own number.

If you are spending $100K a month on ads, you are putting $1.2M through your card every year. At 1% cashback on every dollar, that is $12,000 back annually. If you are at $300K a month, it is $36,000. At $500K, it is $60,000 a year, returned to you automatically, every month, regardless of whether your ROAS was up or down.

That return has nothing to do with how your campaigns perform. It is generated by the act of spending, not the results of it. Whatever number you just calculated in your head: that is what you are currently leaving on the table.

Here is what that looks like across common e-commerce spend levels:

Monthly Ad Spend |

Monthly Cashback |

Annual Cashback |

|---|---|---|

$30,000 |

$300 |

$3,600 |

$75,000 |

$750 |

$9,000 |

$150,000 |

$1,500 |

$18,000 |

$300,000 |

$3,000 |

$36,000 |

$500,000 |

$5,000 |

$60,000 |

Now make it concrete. That $18,000 at $150K/month is a full month of creative production. It is a complete A/B testing cycle across your top three ad sets. It is a part-time performance hire. At $300K/month, $36,000 is a meaningful budget line for influencer testing, a new channel experiment, or a senior media buyer for a quarter.

The cashback does not replace your ad budget. It funds the next thing you were going to have to justify separately.

For a deeper look at how high-volume brands structure their card setup to maximize this return, see how digital agencies earn cashback on ad spend.

Why Most Brands Are Not Capturing This

Most e-commerce brands are not earning meaningful cashback on their ad spend. The reasons are not complicated.

-

They are using a generic business card with a rewards cap. Most standard business cards cap rewards at a spend threshold that made sense for a small business in 2015. A brand spending $150K/month hits that ceiling in the first week of January and earns nothing for the remaining eleven months.

-

They are using a travel or points card that does not optimize for ad spend. Strong general rewards programs exist, but they are built around categories like travel, dining, and office supplies. Ad spend is an afterthought. The effective cashback rate on $2M in annual ad spend through one of these cards is often a fraction of what it appears on the marketing page.

-

They have never separated the card decision from the bank relationship. Most brands use whatever card came with their business checking account. The card was never chosen. It was inherited. Nobody evaluated it as a financial instrument for ad spend specifically.

None of this is a failure of judgment. It is a failure of framing. When you do not think of the card as a financial lever, you do not evaluate it like one.

For a direct comparison of how purpose-built ad spend cards stack up against general business cards, Opal vs. Ramp for agencies breaks down the key differences in limits, cashback, and structure.

What It Actually Takes to Set This Up

The barrier to capturing this return is lower than most brands assume. You do not need a new bank relationship. You do not need to restructure your finance stack. You do not need to get your CFO involved in a months-long evaluation.

You need to replace a card number.

The practical setup looks like this:

-

One virtual card per ad platform. Google gets its own card. Meta gets its own card. TikTok, Amazon, wherever else your spend lives. This gives you per-platform visibility and makes reconciliation automatic.

-

Uncapped cashback on every dollar. The card earning the return cannot have a ceiling. Capped rewards programs are the reason most brands are not capturing anything meaningful at scale.

-

Real-time spend visibility. You should be able to see what each platform is charging, when, without waiting for a monthly statement.

That is the entire setup. The platforms do not care which card number is on file. Swapping it takes minutes per platform. The return starts immediately.

Where Opal Fits

Opal is built specifically for this. It is a charge card designed for brands and agencies running serious ad spend, with 1% uncapped cashback across every platform: Google, Meta, TikTok, Amazon, Snapchat, LinkedIn, and others. No annual fee. No personal guarantee. No hard credit check. Instant limits up to $10M tied to cash flow, not a credit score.

The brands that have made this switch are not doing anything sophisticated. They evaluated the card they were using, realized it was not working as a financial instrument, and replaced it with one that does. The cashback started accruing. The math worked out exactly as described above.

They did not spend more. They just stopped leaving money on the table.

For the full breakdown of how Opal compares to other options in the market, see the best credit card for online advertising.

Your ad spend is already going out every month. The only question is whether it's coming back. See what Opal returns on your current spend volume at opalspend.com.

Frequently Asked Questions

Is cashback on ad spend taxable income?

Generally, the IRS treats cashback earned on business purchases as a reduction in the cost of those purchases rather than as taxable income. This means your ad spend is effectively reduced by the cashback amount for accounting purposes. That said, tax treatment can vary based on your business structure and how the cashback is applied. Consult your accountant for guidance specific to your situation.

Does the cashback rate apply to all ad platforms or just specific ones?

With a purpose-built ad spend card like Opal, the cashback rate applies across every platform where you run ads: Google, Meta, TikTok, Amazon, Snapchat, LinkedIn, Apple, and others. The rate is not category-specific or platform-specific. Every dollar charged to the card earns the same rate, regardless of where it goes.

How is this different from a regular business rewards card?

Most business rewards cards are designed for general business spending and optimize for categories like travel, dining, and office supplies. Ad spend is either excluded from bonus categories or subject to a rewards cap that most high-volume brands exceed quickly. A card built for ad spend has no cap, applies the same rate across all ad platforms, and is structured around the volume levels that e-commerce brands actually operate at.

What is the actual process for switching which card your ad accounts run on?

It is straightforward. Log into each ad platform's billing settings, remove the existing card, and add the new one. Most platforms (Google, Meta, TikTok, Amazon) allow you to update payment methods in under five minutes. With virtual cards, you can generate a dedicated card for each platform before you start, then add them one by one. The entire switch for a brand running four to five platforms typically takes less than thirty minutes.